September 25, 2019

With the world’s largest pig farming industry and generating output value of more than Rmb1trn, China’s industry is nonetheless dominated by a large number of small farms.

Time could be running out, however, for China’s smaller farms as a number of factors support a shift toward large-scale farming. African swine fever could also push the smaller farms out of the industry.

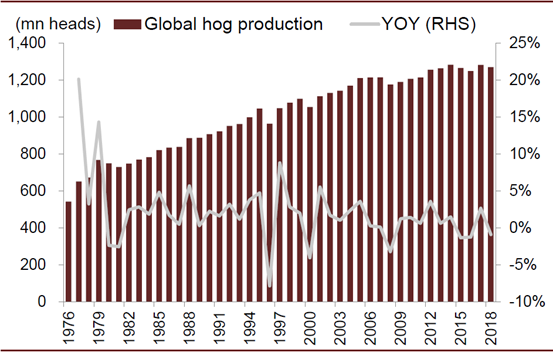

Figure 1: Global hog production at a glance

Source: USDA, CICC Research

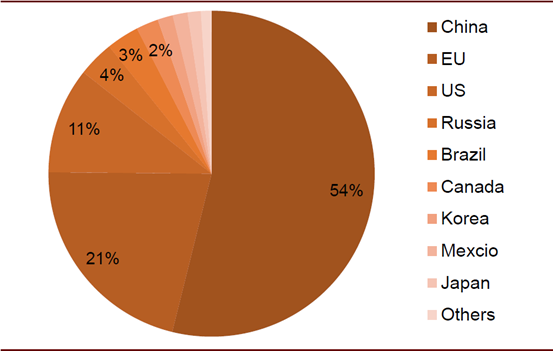

Figure 2: Global pig farming – markets by output (2018)

Source: USDA, CICC Research

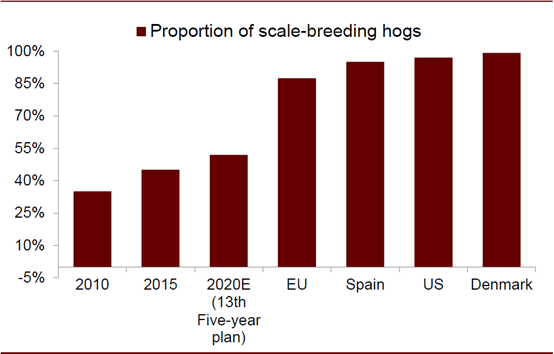

China still has a relatively large number of small pig farms

(i.e. those with annual output of less than 500 pigs)

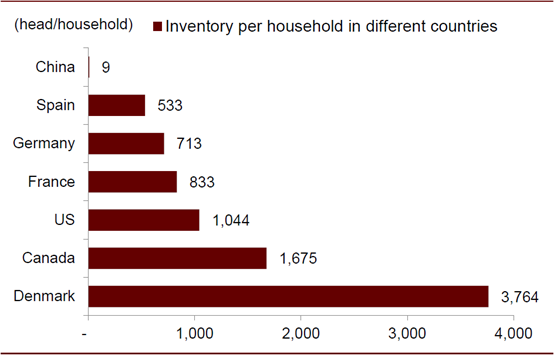

Mid- and large-size farms still account for only half of China’s hog output, well below the 88% in the EU and 97% in the US. Average pig inventory per farm is only nine units in China vs. more than 500 units in the US and Europe.

Figure 3: China – proportion of mid- and large-size pig farms

Source: Ministry of Agriculture, USDA, CICC Research

Figure 4: China – average pig inventory per farm (2016)

Source: USDA, Eurostat, China Animal Husbandry and Veterinary Yearbook, CICC Research

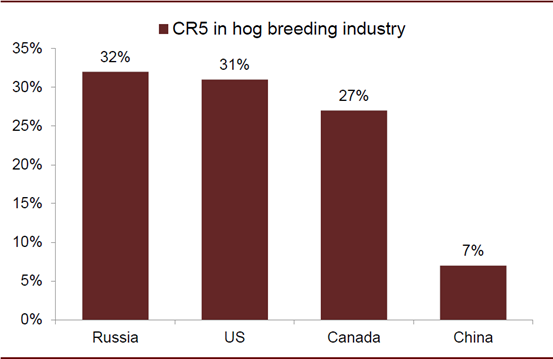

In addition, China’s leading industry players have a smaller market share than their foreign counterparts. For example, the aggregate market share of the top five players in the US (CR5) was 31% in 2018, with Smithfield having an almost 15% market share. In contrast, China’s CR5 is much lower at only 7%, as many domestic players initially did not focus on scale.

Figure 5: China – CR5 in pig farming industry (2018)

Source: Pork Powerhouse, NSSRF, Pig333, corporate filings, CICC Research

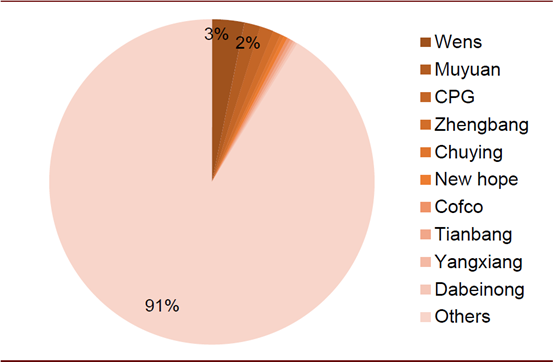

Figure 6: China – hog farming players and their market shares

(2018)

Source: Corporate filings, CICC Research

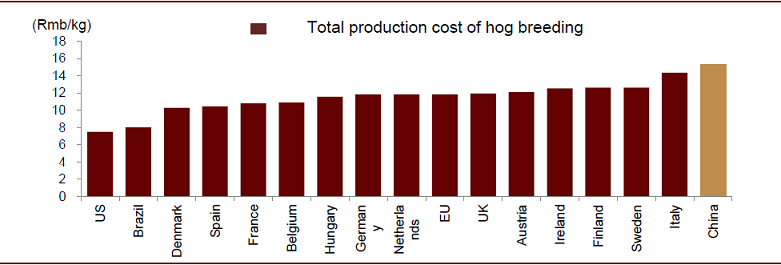

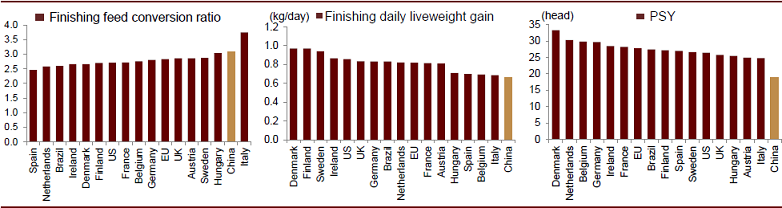

All this could mean there is room for structural improvement in China’s pig farming industry. As for efficiency, China also lags behind its foreign counterparts. Specifically, China’s pig feed utilization is inefficient, while the daily average liveweight gain in China is only 661 grams vs 971 grams in Denmark, and the number of pigs weaned per sow per year (PSY) in China is also much lower than in the US and Europe.

Figure 7: Hog farming industry – total cost in China and other

countries (2017)

Source: AHDB, Cost and Benefit of Agricultural Products, CICC Research

Figure 8: Hog farming industry – efficiency in China and other

countries (2017)

Source: AHDB, Cost and Benefit of Agricultural Products, CICC Research

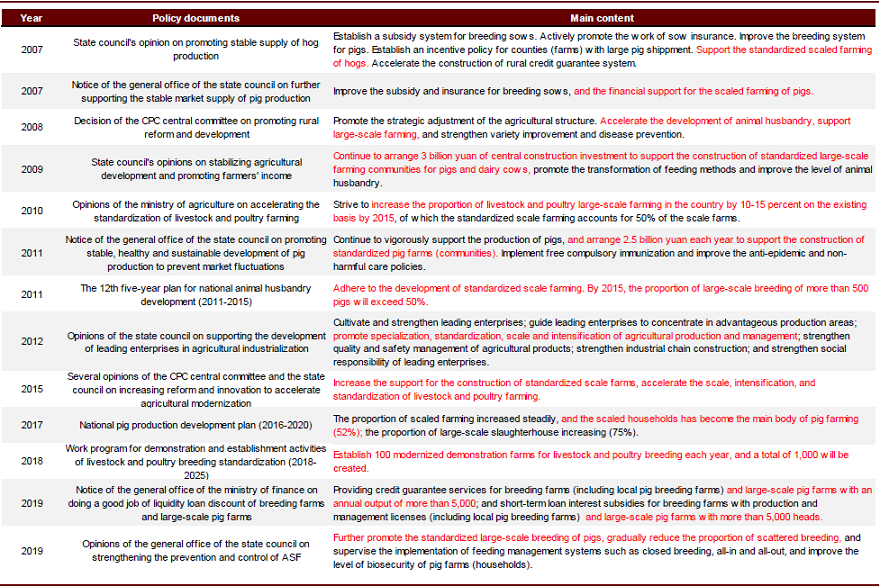

Policy support for large pig farming companies

China’s policymakers have over the years encouraged the country’s pig farmers to grow in scale, and also promoted industrial transformation and upgrading to improve efficiency. Subsidies have also been made available to pig farming companies that meet specific scale requirements.

Figure 9: Summary of policies designed to encourage scale

expansion

Source: State Council, Ministry of Agriculture, CICC Research

The policies appear to be working. The number of companies with annual output of more than 50,000 hogs expanded most rapidly, surging five times to 311 in 2016 from 50 in 2007. According to China’s hog production plan for 2016–2020, the country plans to raise the proportion of mid- and large-size pig farming companies to 52% in 2020. Future policies could further support large-scale pig farming.

Figure 10: China’s pig farming industry – growth in different

categories of pig farms (2007–2016)

Source: China Animal Husbandry and Veterinary Yearbook, CICC Research

ASF could also push the industry toward greater scale

African swine fever (ASF) has been disruptive to China’s pig farming industry, and a large number of small farms have exited the market as they suffered heavy losses. While mid- and large-size players have also been affected by ASF, they are better equipped to handle the situation as related costs should be lower for them, thanks to stronger financial management and having more advanced facilities.

Tougher environmental regulations also put pressure on smaller

pig farms

A large number of small pig farms in China have closed amid the tougher environmental regulations in recent years. In the past, small pig farms would discharge pollutants illegally, allowing them to have net margins similar to the large farms. However, with the tougher regulations, small farms are required to install environmentally friendly facilities. With the leveling of the playing field, large pig farming companies have started to benefit from their cost advantage, and their net margins are now almost 15ppt higher than for their smaller counterparts.

Figure 11: Profitability of small pig farms and large farming companies

Source: Cost and Benefit of Agricultural Products, CICC Research

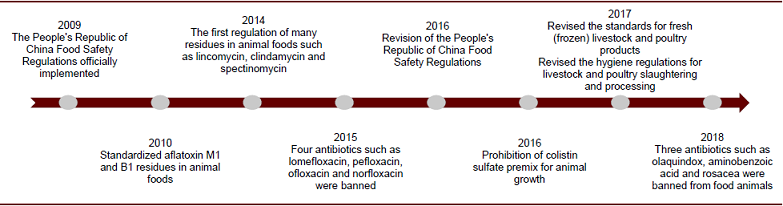

Improving food safety system could promote industry upgrade

China is improving its food safety system and large farming companies have taken steps to ensure their feed is antibiotic-free and that their products are traceable. They are also attempting to expand into the downstream slaughtering and safe food markets. This could potentially give them a greater advantage as China steps up its efforts in quality certification.

Figure 12: China’s food safety system has been improving

Source: China National Center for Food Safety Risk Assessment, CICC Research

For more details, please see our report Pig

farming industry to experience high growth published in September 2019.