June 4, 2019

Chinese travelers are going on trips in record numbers. More and more are choosing to spend their holidays abroad and business travel is commonplace.

This is all part of China’s great economic transformation that has seen a significant rise in incomes and a transition toward a consumption-based economy. Chinese airlines have directly benefitted from this growth in travel and have been battling for years to capture this burgeoning opportunity.

Industry conditions for Chinese airlines are poised to further improve, following a series of developments.

Market consolidation

Chinese airlines, like their US counterparts, have undergone a wave of consolidation and could see a similar growth story.

Consolidation in the US

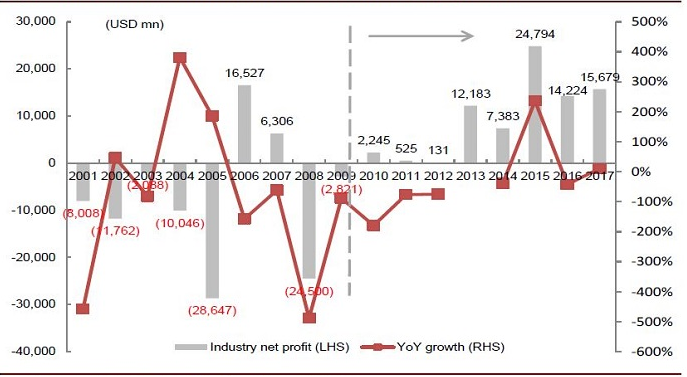

In the US, airline consolidation significantly improved industry profitability. It paved the way for its airline industry to turn profitable in 2010, which has remained so for 9 straight years.

Figure: Market consolidation improved US airline industry’s profitability

Note: YoY growth in 2013 was 9,166% and is not shown in the figure. Source: US Bureau of Transportation Statistics (BTS), CICC Research

Note that it took years before the US industry stabilized and took on its current form. The industry has witnessed more than 10 M&A deals since 2000, such as United Continental’s acquisition of Continental Airlines in 2010, and United Airlines’ merger of US Airways and AMR in 2013. As a result, the three largest airlines saw their market share by revenue passenger miles (RPM) increase from 59% in 2010 to 74% in 2012, and stayed between 68% and 74% over 2012 to 2018. RPM and RPK are industry terms for the number of miles or kilometers traveled by paying passengers.

Figure: M&A deals in the US airline industry

Source: Airlines for America, CICC Research

Consolidation in China

Similarly in China, consolidation was also a common theme. In 2002 to 2003, China National Aviation Corporation and China Southwest Airlines were reorganized into Air China; China Northwest Airlines and Yunnan Airlines became China Eastern Airlines; and China Northern Airlines and Xinjiang Airlines became China Southern Airlines.

In the wake of the 2008 financial crisis, China Eastern Airlines, China Southern Airlines and Air China – “the Big 3” – suffered losses of Rmb13.9bn, Rmb4.8bn and Rmb9.1bn respectively, which triggered another round of market consolidation.

China Eastern Airlines merged with Shanghai Airlines in 2010 and Air China acquired Shenzhen Airlines in 2013, increasing the Big 3’s market share from 68% in 2012 to 73% in 2013.

Figure: Four major airline groups in China

Source: Corporate filings, CICC Research

Signs of improvement for Chinese airlines

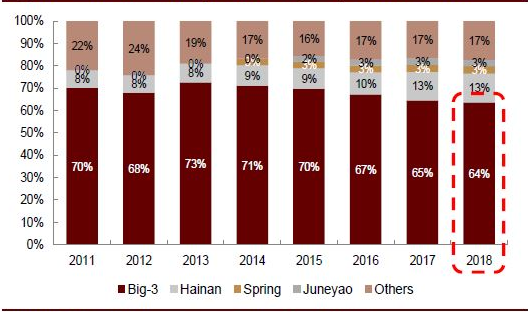

Despite the consolidation in both markets, industry concentration is still higher and more stable in the US, which could mean there is room for improvement for Chinese airlines.

For comparison, while the market share of the US’s three largest airlines by revenue passenger kilometers (RPK) remained above 68% in the past 3 years, China’s Big 3 saw their market share drop to 64%. But it appears to have stabilized at that level, dropping just 1ppt from 65% in 2017, which could potentially signal a turning point for the Chinese industry.

Figure: Market share of China’s Big 3 by RPK stabilized

Source: CAAC, Wind Info, Corporate filings, CICC Research

In addition, reforms in the Chinese industry have had a positive impact and could pave the way for growth.

Reforms in China’s airline industry

The Civil Aviation Administration of China (CAAC) introduced a policy in 2H17 to control the growth of available seat kilometers (ASK), an industry term for measuring an airline’s carrying capacity for generating revenue, i.e. the number of seats available multiplied by the number of kilometers flown.

After CAAC introduced the policy, overall ASK growth dropped 1ppt from 2017 to 12.5% YoY in 2018, which helped improve supply-demand conditions.

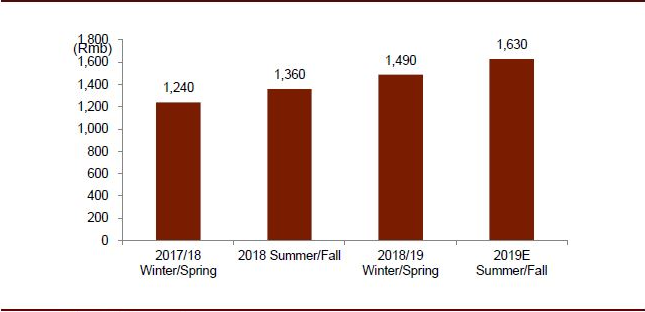

In addition, the deregulation of airfares has allowed Chinese airlines to raise ticket prices on domestic routes at the end of April 2018, which further strengthened the industry by allowing airlines to pass on rising costs to passengers.

This came after the CAAC issued a notice in 2015 requiring the full liberalization of airfares in 2017. Furthermore, a market-oriented pricing system and transparent price monitoring system would both become available in 2020.

Figure: Full-economy-class fares on Beijing-Shanghai flights jumped 20%

Source: CTrip, CICC Research

Positioned to take-off

Chinese airlines have undergone a period of fierce competition and consolidation, and there appears to be signs that the industry is improving.

Providing further support is the decision by China’s State Council to slash by 50% the levies that airlines have to collect on behalf of the government for the Civil Aviation Development Fund, slated to take effect July 1, 2019.

This bodes well for the industry and could directly reduce costs for airlines. It may also provide room for airlines to further raise ticket prices.

For more details, please see our report Airlines in China: competitive landscape improves, airfares turn around published in April 2019.