January 26, 2021

Online game market: The trend toward higher quality;

leading game companies boost R&D

China’s game market saw a boom

last year as people spent more time at home amid the COVID-19 pandemic.

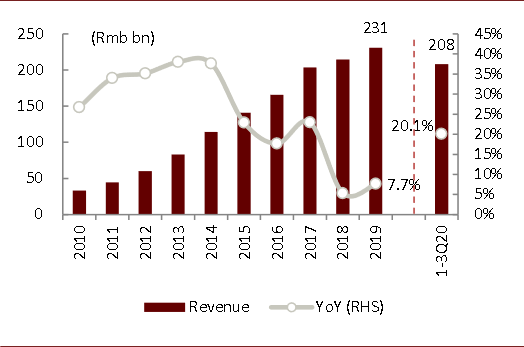

Revenue generated by China’s game market grew 20.1% YoY to Rmb208.02bn over 1–3Q20,

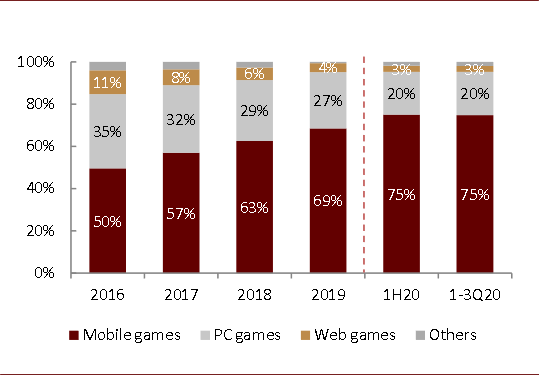

with revenue from mobile games accounting for a 75% share. There was a rise in

both the number of active gamers and the amount of time spent on playing games.

Figure 1: Revenue generated by China’s game market (2010–3Q20)

Source: CNG, China

Audio-video and Digital Publishing Association, IDC, CICC Research

Figure 2: Breakdown of China’s

game market (2016–3Q20)

Source: CNG, China

Audio-video and Digital Publishing Association, IDC, CICC Research

Overview

The number

of people playing mobile games has reached 651mn, after having risen 0.94% QoQ in 1Q20, 0.25% QoQ in 2Q20 and 0.51%

QoQ in 3Q20.

While this number could gradually slow and stabilize, it is worth noting that

even after average revenue per user (ARPU) generated by mobile games grew 36.4%

QoQ in 1Q20, it still rose 2.6% QoQ to Rmb78 in 3Q20, which could indicate

strong growth potential.

Going forward, ARPU generated by mobile games could continue to grow and the

mobile game market may further expand. This is as users are increasingly

willing to pay for games and the quality of games is improving.

Regulatory

approval of licenses for online games normalized; policies to encourage quality

games

Over January 1–December 2, 2020, National Press and Publication

Administration (NPPA) issued 21 batches of licenses for domestic online games

(1,227 licenses in total) and four batches of licenses for imported online

games (98 licenses in total). On average, NPPA issued one to two batches of

licenses (about 50–70 licenses per batch) for domestic online games per month, even

during the COVID-19 pandemic.

In addition to issuing new licenses for games, NPPA has also revoked licenses

for 19 existing games that violated related rules since September, in an effort

to strictly control the quality of games. Meanwhile, NPPA released information

about changes of operators, publishers and names of some games that gained

regulatory licenses over 2015–2020.

The trend toward higher quality games

The number of regulatory licenses for online games has declined as gamers pay

greater attention to the quality of games.

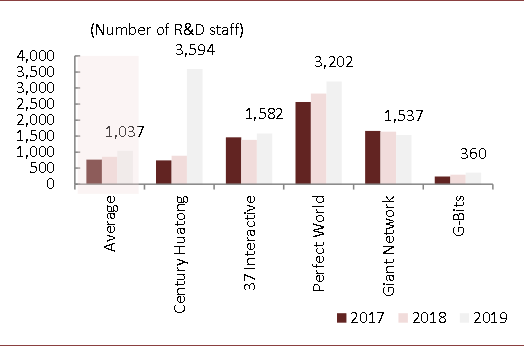

The emphasis on quality could mean a trend toward higher R&D spending by

game developers. Average R&D spending of leading game development companies

in the A-share market grew at a CAGR of 24.4% from Rmb0.28bn in 2017 to

Rmb0.44bn in 2019, and rose 29.2% YoY over 1–3Q20.

Furthermore, their average number of R&D employees grew at a CAGR of 16.4%

from 766 in 2017 to 1,037 in 2019. Their R&D spending per R&D employee

rose from Rmb397,154 in 2017 to Rmb443,036 in 2019.

Figure 3: The

number of R&D employees has risen at most leading listed game companies

Note: Companies in the above figure are top 5

companies by market cap in the CITIC game sector index as of November 6, 2020;

R&D employees of Century Huatong increased markedly in 2019 due to the acquisition

of a game company; R&D employees of Sanqi Interactive decreased in 2018 due

to the disposal of auto parts business

Source: Corporate filings, CICC Research

Competitive landscape

Data from Analysys shows that the combined market share of Tencent and

NetEase stood at 69.8% in 1H20, slightly higher than in 1H19. It is worth

noting that revenues and recurring net profits of some leading game companies

have achieved higher-than-average growth.

Going forward, leading game companies could potentially see their market share

rise further, as they continue to increase R&D spending and improve the

quality of their titles.

For more details, please see our report 2021

outlook: Content, platforms, technology innovation to fuel growth published

in January 2021.