October 23, 2020

In the 21st century, rapid development of the digital economy has facilitated

production and made people’s daily lives more convenient via online transactions,

logistics tracking, mobile payment, and telecommunication.

The digital economy is playing an increasingly important role in the national

economy. While there is no widely accepted definition, the term “digital

economy” generally refers to economic activities based on digital operations,

information technology and telecommunication technology.

The COVID-19 outbreak in early-2020 accelerated development of the digital

economy. To contain the pandemic, most countries imposed restrictions on social

gatherings and the movement of people to varying extents.

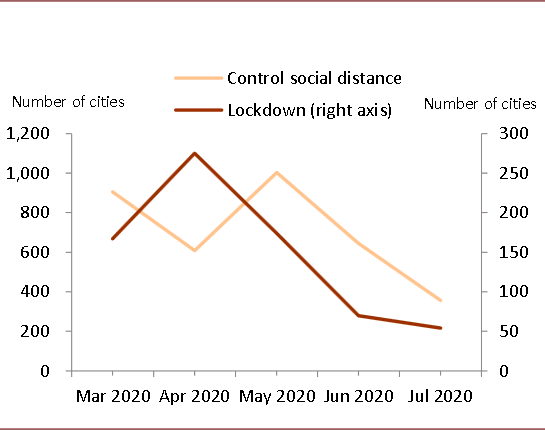

At the peak of the pandemic earlier this year, around 1,000 cities across the

world implemented social distancing rules at the same time, and over 250 cities

were locked down. Restrictions on social contacts forced many companies to

switch to online interactions with employees and clients, and digitalization

became the key to maintaining business operations.

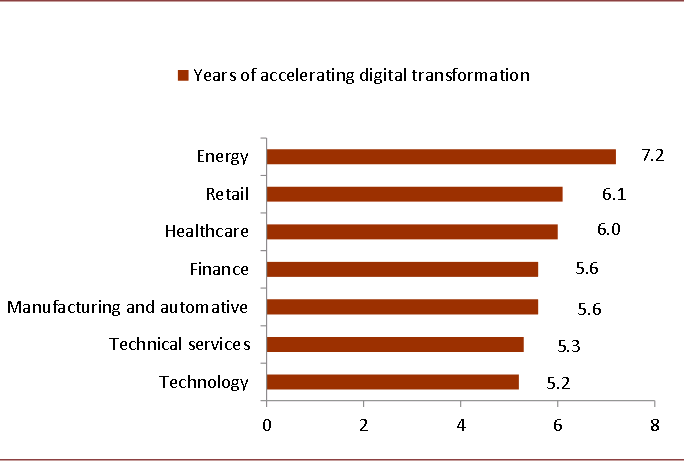

To improve competitiveness, many companies significantly accelerated the

implementation of digital strategies. A survey among 2,569 companies globally

shows that the COVID-19 outbreak brought forward the global digitalization

process by at least 5–7 years.

Figure 1: Number of cities implementing social

distancing rules and imposing lockdowns

Source: ACAPS, CICC Research

Figure 2: COVID-19 accelerates corporate digital

strategies

Note: The data is based on Twilio’s survey about

corporate digitalization amid COVID-19 among 2,569 entrepreneurs in the US, UK,

Germany, Australia, and Japan.

Source: Twilio, CICC Research

Platform economy: A new business model

The platform economy represents the

most typical business model and an important driver of value creation in the

digital economy.

Traditional business platforms are common – shopping malls are platforms that

connect consumers with producers, while talent centers are also platforms that

connect job seekers with recruiting companies. However, these platforms require

physical space and connect a relatively limited number of people.

The platform economy, on the other hand, comprises digital platforms based on

digital hardware and technologies such as data collection and data analysis. It

can reduce physical space restrictions and connect a wider range of people.

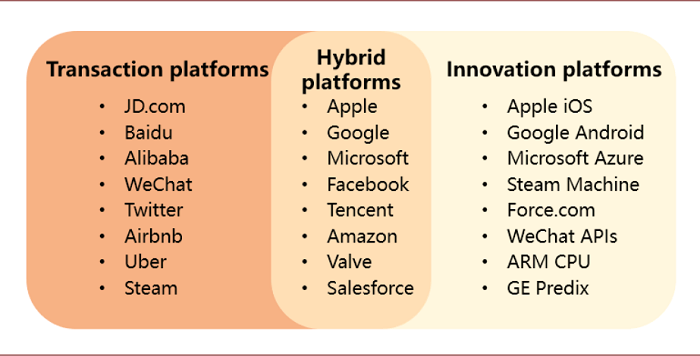

Figure 3: Based on different business types, digital platforms can be

divided into three categories

Source: The Business of Platforms (Harper Business, 2019),

CICC Research

A “winner-takes-all” situation?

As the platform economy grows rapidly, strong platforms tend to

monopolize the market because the platforms’ strengthening network effect “locks

in” users and increases their social and welfare costs of switching to other

platforms, which creates a “winner-takes-all” situation.

At present, giant platform companies already have large user bases and strong

network effects. These companies could have an increasingly strong “lock-in

effect” on users as they improve their technologies, understand user

preferences more accurately, and create more value for users.

Furthermore, strong platform companies develop their own ecosystems as they

integrate relevant peripheral businesses onto their platforms, provide support

for these businesses, and obtain feedback from clients. Thus, strong platforms

create a value network in which multiple transactions are matched and diverse

participants complement each other.

When platforms grow to a certain degree, building a comprehensive ecosystem

leveraging economies of scope will create new and dynamic growth drivers and

support sustained expansion of platforms, in our view. For example, Amazon

integrates its e-commerce, entertainment, finance, and marketing management

businesses onto its cloud computing-based platform, creating a platform

ecosystem.

Service trade to become a new growth driver

With regard to international trade in economics, goods and services are

usually divided into two categories: tradable and non-tradable.

Generally speaking, goods are tradable. For example, refrigerators,

air-conditioners, and mobile phones made in China can be exported to Europe,

and airplanes made in Europe can be exported to China.

However, services are generally regarded as non-tradable. This is because service

activities often require interaction between people, but people cannot move

freely across borders.

However, digital economy applications have reduced the cost of remote

communication, so that the tasks or transactions that used to require interaction

between people can now be done without interpersonal contact.

This is particularly important amid the COVID-19 pandemic. The digital economy

partly overcomes the barriers to the movement of people, making services more

tradable. The future development of the digital economy may go beyond our

traditional knowledge.

Service trade can enhance

productivity

Public policies can play an important role in boosting development of

the service sector. The government can enhance the tradability of the service sector

by promoting infrastructure construction for the digital economy.

The COVID-19 outbreak has prompted governments around the world to step up

construction of broadband, 5G, and other digital infrastructure to improve

efficiency. On the other hand, public policies can encourage competition,

reduce monopoly, and make it easier for the service sector to integrate with

the digital economy. Such policies may enhance the openness of internet

platform companies such as Facebook, Google, Tencent, and Alibaba. To some

extent, these companies have already begun to monopolize the industry.

Whether they will become contributors or obstacles to innovation in the service

sector depends on how public policies guide them.

For more details, please see our report New

structures, new issues: Macro and theoretical analysis of the digital economy published in October 2020.