China’s new asset management rules have triggered capital and asset reallocation, and reshaped the landscape of the asset management industry.

This is part of the evolution of the industry, which has developed over the past two decades.

Top-tier securities firms are now poised to benefit, and the race is on to capture new fund inflows into the asset management industry.

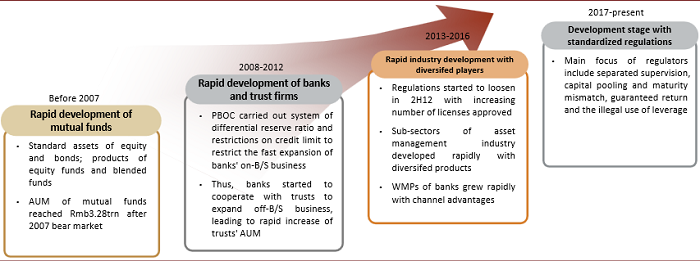

Figure 1: Development of China’s asset management industry

Source: Annual Report on Development of China’s Asset Management Industry, CICC Research

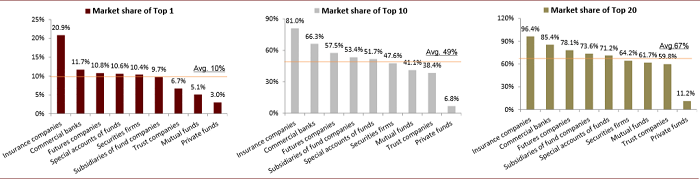

Figure 2: Revenue breakdown vs AUM market share

Source: AMAC, China Trustee Association, China Banking Wealth Management Registration Center, CBIRC,

Corporate filings, CICC Research

Overview

Revenue of China’s asset management industry reached Rmb433.1bn in 2018 (implying average management fees of around 0.45%), with almost 90% from PE funds (Rmb127.1bn), fund management companies (Rmb96bn), commercial banks (Rmb88.2bn) and trust firms (Rmb78.2bn). In terms of management efficiency, average revenue from asset management business reached Rmb1.2bn for trust firms, Rmb1bn for insurers, and Rmb700mn for fund management companies, all much higher than the average revenue of other asset management firms.

In the markets for each type of asset management company, the average share (measured by revenue or AUM) is 10% for the largest player, 49% for the top-10 and 67% for the top-20. The market for asset management firms owned by insurers and banks has a much higher concentration ratio than the market for other types of asset management firms. In contrast, the market for asset

management service operated by PE funds has a much lower concentration ratio.

Figure 3: Market concentration is higher among insurers and banks’ asset management firms, and lower among PE funds

Note: Data as of 2018; market share for insurance asset management firms and trust companies based on revenue; market share for other firms based on AUM.

Source: AMAC, China Trustee Association, China Banking Wealth Management Registration

Center, CBIRC, Wind Info, CICC Research

The scramble for important sources of new fund inflows

For China’s asset management industry, the main sources of funds are from individuals, financial institutions, governments, enterprises, and pension funds.

Investment demand from mid- and high-net-worth individuals

Going forward, a possible future important source of new funds could come from wealth management demand from mid- or high-net-worth individuals, which is a segment that is underserved compared to developed economies, thus providing a sizeable opportunity for leading industry players.

According to a survey by McKinsey, the aggregate wealth of Chinese individuals may reach about Rmb137trn in 2019, of which 20mn mid- and high-net-worth individuals have total investable assets of Rmb69trn.

The assets of mid- and high-net-worth individuals are now mainly managed by private banks, trust firms, third-party wealth management institutions, and top-tier securities firms. The asset management market for mid- and high-net-worth individuals remains promising, in contrast to long-tail retail and wealth management markets that face intense competition. McKinsey’s survey shows that only 20% of wealthy individuals in China now have investment advisors, far below the proportion of more than 50% seen in developed economies.

This provides a sizeable opportunity for asset management firms. A 1% market share of China’s 20mn mid- and high-net-worth individuals that have total investable assets of Rmb69trn would mean Rmb0.7trn in AUM and 200,000 customers. This means China needs 1,000 professional investment advisors, assuming an advisor serves 200 wealth management customers, which is the average level seen in mature markets.

Figure 4: Mid- and high-net-worth individuals are served mainly by leading private banks and top-tier brokers

Source: Corporate filings, CICC Research

Figure 5: Brand and asset allocation ability are the most important factors for individuals when selecting a wealth management firm

Source: BCG, CICC Research

Investment outsourcing demand from China’s pension

management institutions

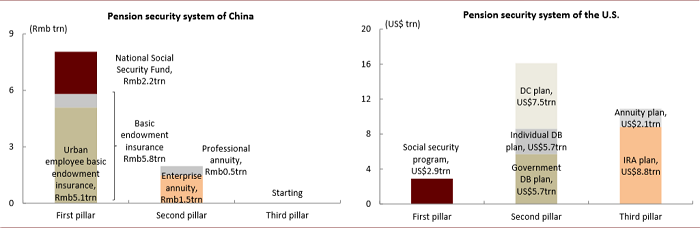

Another source of funds could come from investment outsourcing demand from China’s pension management institutions; in 2018 China’s pensions totaled Rmb10trn, only 5% of the level seen in the US.

China’s total pensions (including basic old-age insurance, social security funds, enterprise annuities and professional annuities) accounted for only 11% of the country’s GDP in 2018, much lower than levels seen in mature overseas markets. Pensions under outsourced management totaled Rmb3.2trn, constituting 32% of the total pensions in the country. Looking ahead, it appears that

China’s total pensions and proportion of pensions under outsourced management both have large growth potential.

Figure 6: China’s pension size and structure both lag the US

Source: SSF, MOHRSS, NBS, Investment Company Institute, US Department of the Treasury, CICC Research

For more details, please see our report China’s asset management industry: a US$10trn market published in December 2019.